In Part 1 of this series we asked a simple question: is it better to have a legacy pension, or a well-funded 401k?

We proved, mathematically, that a 401k is at least as good as a legacy pension plan under very conservative assumptions. Under still very reasonable circumstances, the potential value of a 401k blows a legacy pension out of the water. This is before remembering that 401k plans are protected from a company’s creditors in case of bankruptcy, and a pilot can pass the entirety of the funds in a 401k plan on to their heirs. Neither of those two facts applies to pension plans.

In their recently failed Tentative Agreement (TA1), current pilots at FedEx were offered the opportunity to freeze their pension benefits and switch to a Market Based Cash Balance Plan (MBCBP) going forward.

Based on Part 1 of this post, it appears that any pilot with more than 25 years until Age 65 would benefit from making that switch. Realistically, since switching pilots would keep a portion of their pension benefits, it’d likely make sense to switch with even fewer than 25 years remaining.

The point where switching makes sense moves later and later in life, depending on whether a pilot feels comfortable using a 4% Rule to determine spending in retirement, or wants to use a slightly more permissive percentage. (As always, I strongly recommend you consult a Certified Financial Advisor for help making this decision.)

All that said, some key characteristics of the current and proposed retirement options at FDX gave me pause. I’ll hold short of expressing a qualitative assessment other than to say that the current 9% Direct Contribution (DC) at FDX falls well short of the standard of “industry leading” that union bosses and corporate execs love to cite.

In this post, I’ll use math to prove my position and highlight some things that I’d certainly be advocating for if I were approaching contract negotiations at purple or brown.

The 9% Purple Pay Cut

In addition to the legacy pension, or “A-Plan,” we discussed in Part 1, the FedEx pilots have a 401k often referred to as the “B-Plan,” “Pilot Retirement Savings Plan,” or “PRSP.”

This plan is partially funded by a 9% Direct Contribution (DC) made by FedEx each month. While many employers match an employee’s personal 401k contributions up to a designated limit, the 9% FDX DC (and similar DCs at other major airlines) are nonelective contributions. This means these funds are paid into each pilot’s 401k account every month, no matter whether the pilot contributes any personal funds or not.

For 2024, the maximum amount of money per year that can be contributed to any person’s 401k account is $69,000, with pilots over age 50 allowed to make a catch-up contribution of up to $7,500. If the FDX DC doesn’t reach that annual threshold ($69K/$76.5K) a pilot can make individual contributions of up to $23,000 (or $30,500 over age 50) to cover some or all of the difference.

(Many plans also offer a “backdoor” option where a pilot can contribute after-tax money to their 401k. Those funds can be converted to Roth dollars using what is sometimes referred to as the “mega backdoor Roth.”)

This setup creates a problem for purple pilots every year. They have to guess, early in the year, how much to contribute to their 401k plans to avoid losing out on any of that 9% DC money because of too much personal contribution early in the year. There are resources to help make this guess, but should it have to be that difficult?

Unfortunately, another IRS limit applies to 401k plans for many pilots. Under section 401(a)(17), a company can only make Direct Contributions on the first $345,000 of a person’s income in 2024 (up from $330,000 in 2023). With a top pay rate at $335/hr, it’s likely that many FedEx pilots reach this limit each year. The UPS pilots’ top pay rate is $401/hr, while top pay at Delta & United will soar to $483/hr in 2026. It’s likely that FedEx pay rates will climb to at least match their peers, meaning that even more purple pilots will hit the 401(a)(17) income limit each year.

When this annual income limit is reached, their company is required by law to stop contributing to their 401k account for the rest of the year. Okay, fine…right?

The question most purple pilots I know gloss over is: How does this work for their peers at other airlines?

At American, Delta, and United, company DC used to be 16%. It climbed to 17% at the start of 2024, and will climb to 18% at the start of 2026.

Our industry’s freight pilots have accepted a much lower DC percentage because they are the only pilots with legacy pension plans. Common wisdom accepted the pension as infinitely superior to a 401k, so a 9% DC was almost viewed as a bonus. Who cares if that bonus gets cut off part way through the year, right?

However, it’s critical to note these other companies don’t stop paying pilots that DC percentage just because they’ve reached the IRS’s 401(a)(17) income limit, or because a given pilot’s account contributions hit the annual $69K limit.

At United, any excess funds used to get contributed to a Retirement Health Account, or RHA, similar to an HSA. Under their new contract, United pilots will be able to choose whether those 401k excess funds continue going to their RHA, or to a new MBCBP. Ideally, they’ll get to make that election each year.

At Delta, those excess funds used to be paid as taxable cash in a pilot’s regular paycheck. Sometimes referred to as “cash over cap” or “spill cash.” It’s tough to argue with the cash hitting your checking account increasing by 17% at some point in the year! Under their new contract, a MBCBP at Delta protects an unlimited quantity of 17% DC dollars each year. Current Delta pilots got a one-time choice to join the MBCBP or only ever get spill cash. Future pilots will all participate in the MBCBP.

The key here though is that these airlines don’t just stop giving the pilot their 17% DC because that pilot’s income hit the IRS limit. They’ve found legal ways past those limits to continue compensating their pilots.

In effect, this means that the highest earning pilots at purple get a 9% monthly pay cut at some point every year.

All other judgment aside, it’s fair to say that this is not an “industry leading” contract provision.

The 20% Purple Pay Cut

Although any purple pilot is likely to suffer from that 9% pay cut at some point in their career, the situation would have gotten worse under the proposal in TA1.

This proposal essentially ended access to the pension to future pilots, forcing them into the MBCBP instead. It also gave current purple pilots the option to freeze their current pension benefits with a raised Final Average Earnings (FAE) cap, and transition to the new MBCBP moving forward.

The TA offered an 11% DC to the MBCBP in parallel with the 9% DC to a pilot’s 401k plan.

On one hand, this sounds good. A 20% DC effective immediately seems to beat peer DCs that won’t even reach 18% until 2026. However, the TA also carried over the provision that all contributions would stop at the 401(a)(17) income limit of $345,000.

Bottom line: this isn’t necessary. Yes, at that income level, the company can’t make any more contributions directly to a 401k. However, they could have agreed to start paying spill cash, or set up a VEBA. They did set up a MBCBP, but in this case they completely missed the point.

The pilots at Delta, United, American, and Southwest didn’t add MBCBPs because they wanted a different kind of retirement vehicle. The MBCBP is an arguably worse vehicle than a 401k, and completely unnecessary for savvy investors. The only reason for a MBCBP to exist is to make (unlimited) room in a tax-advantaged account for a company’s contributions to continue flowing after a pilot’s income has reached the $345,000 per year threshold, or after the pilot’s personal 401k contributions have helped total contributions for the year hit the $69,000 limit.

The MBCBP in FDX TA1 stops at the exact point where it would start to mean something. They didn’t choose 9/11% by accident. 9% of $69K is $31,500, and 11% of $69K is $37,950. Put together, these equal $69,000.

Those numbers were specifically selected to ensure that company DC doesn’t go one penny beyond the lines conveniently drawn by the IRS. Those lines make stopping there sound reasonable. They’re federal law, after all. Right?

And yet, several other major airlines have found ways cross those lines and increase their pilots’ overall compensation.

The 9/11% proposal (an inauspicious choice of figures for airline pilots) essentially switches to a 20% monthly purple pay cut.

An annual 9% pay cut seemed okay-ish when it was just gravy on top of a lucrative pension. Increasing that pay cut to 20% without the benefit of the pension making up the difference is a bad deal for purple pilots.

This definitely would have failed to meet any possible definition of “industry leading.”

If I were a pilot providing feedback to union leaders at a purple or brown airline, I’d include as one of my top priorities wanting the same DC policies as the rest of our industry. The DC shouldn’t stop at some convenient limit. If IRS limits are reached, the DC continues as contributions to an RHA or VEBA, spill cash, or contributions to a MBCBP.

Ideally, individual pilots would get to choose between all three of those options each year. IRS rules likely prevent this choice, though United’s contract directs their MEC and the company to seek approval for an annual election between either their RHA or the MBCBP. We should all hope this gets approved!

More Pension Pilot Math

Since this is Pilot Math Treasure Bath, and since I was building a pension-related spreadsheet based on this situation anyway, I decided to add a tab for calculating the monetary difference between the retirement setup proposed in FDX TA1 and what their peers get.

This calculator is straightforward. It compares pilots with the exact same amount of regular pay at FedEx and Delta. It allows for the Delta pilot to specify a personal contribution if they want to maximize tax-advantaged savings in a given year.

The FedEx pilot can specify a personal contribution, but might as well not in many cases. With the company DC cutting off once the $69,000 annual contribution limit is reached, there’s no point. The calculator warns you if the personal contribution you chose would exceed the annual IRS income limits for the FedEx side. I recommend not violating those limits. (Sorry, I didn’t program something fancier here. The formulas were already getting a little hairy. I really need to learn Python.)

The calculator asks you to estimate your overall current tax rate because it only compares current compensation. It asks your age to know (automatically) whether you’re eligible for $7,500 in catchup contributions.

The results determine which plan is better at that income level with those inputs. That difference is quantified in Total Annual Compensation. The calculator also shows which scenario has the greatest tax advantages.

Specific Scenarios

At incomes below the IRS limit of $345,000, and without personal contributions, the FedEx setup has a clear advantage. Up to that point, the 20% FedEx DC will always beat Delta’s current 17% DC, and it protects more money from taxes.

However, if both pilots make significant personal contributions, things change. The FedEx pilot can only contribute a maximum of $19,000, but the Delta pilot can easily make double the contribution. This protects an extra $11,500 from taxes, narrowing the difference in effective compensation to less than $5,000, reducing the impact of the 3% DC difference between the two companies.

This same basic advantage continues to a break even point just under $406,000 if neither pilot makes any personal contributions.

However, the Delta pilot retains the ability to make significant tax-advantaged contributions that ceased to be an option for the FedEx pilot.

Note that in this last scenario, basic income stayed equal for our two pilots. However, the tax advantages for the Delta pilot are significant, meaning overall effective compensation favors Delta.

At higher income levels, Delta’s plan has clear advantages. In contrast to the 20% purple pay cut, the 17% Delta DC continues going toward our pilot’s total compensation. If that pilot chooses to make some personal 401k contributions, they are able to gain tax advantages for far more of their money, meaning they enjoy big tax savings, and widening the effective compensation difference.

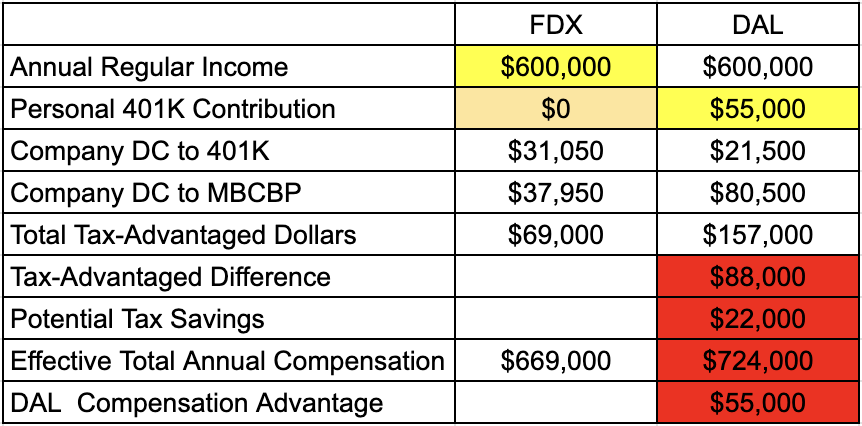

Finally, we’ll consider a more extreme case. Whether flying trips for premium pay, or flying as a Line Check Pilot with a top line pay rate of $483 per hour and an LCP override of an additional $144 per hour for a total rate of $627 per hour, $600,000 in annual income is reasonably attainable for a senior Delta pilot under their current contract. This is tougher for a FedEx pilot at current pay rates, though still possible. They’re likely to get pay increases on par with their industry peers, making this level of income equally attainable:

In this scenario, the Delta pilot’s ability to front-load personal contributions into their 401k maximizes money into their MBCBP for the year, and wins them a staggering $157,000 in tax-advantaged dollars.

By using Traditional (instead of Roth) contributions, this would save the pilot an extra $22,000 in taxes this year. Between that and their 17% DC continuing to pay out long after the 20% purple pay cut of our freight dawg, the Delta pilot enjoys an extra $55,000 in effective overall compensation this year.

Soft pay is critical in airline pilot contracts. In this case, two seemingly small provisions make a five-figure difference every year. First, the Delta pilot’s DC doesn’t cut off at an arbitrary and unnecessary point. Second, the fact that all excess money spills into a MBCBP allows the Delta pilot to maximize tax advantages by front-loading large personal contributions.

So What?

The intent of this project is not to disparage one contract, or even one failed Tentative Agreement. This is merely a mathematical examination of the implications of a given proposal.

Now that TA1 is ancient history, the FDX MEC will reach out to their pilots for input on what a future TA2 has to include for it to pass. The UPS union leaders are also likely seeking input from their pilots in preparation for negotiations that could start later this year.

I hope this case study illustrates the value of a couple key provisions in one contract that may be attainable in others thanks to Captain Dave Behncke’s grand strategy of pattern bargaining.

I suspect that these contracts will continue a trend of seeking to end the pensions at these companies, giving current pilots the option to transition to a MBCBP. Based on Part 1 of this series, and our comparison here, there may be more pilot support for this trend than traditional opinion might suggest.

Even just considering the IRS contribution limit of $69,000 per year, it will likely take fewer than 25 years for a 401k plan’s value to match or exceed the value of a legacy pension. If you really want to see some big numbers, use the FDX Case Study tab from this calculator to find out how much money you could put into tax-advantaged accounts if you include some personal contributions under contract rules like those at Delta. (It doesn’t take much to get that number above $90,000 per year). Then, use that number for your Annual Contribution amount on the Pension Calculator tab from Part 1 of this series.

(Spoiler alert: these numbers put any legacy pension to shame).

I strongly recommend discussing the implications of these calculations with a Certified Financial Advisor. If you do, they may help you frame the inputs you give your union reps on what kinds of provisions you want to see in your next contract.

I wish you all the best in those efforts. I’d be thrilled to walk an informational picketing line in your support, though I hope your management doesn’t let things get that far.

This post’s featured image came from Levi Meir Clancy on Unsplash.

One thought on “Airline Pensions Part 2: Case Study”