Apparently, some pilots have gotten themselves very worked-up over the fact that US Department of the Treasury rules state that if an employer offers something like our MBCBP, all members of a given employee group must be included. Some pilots plan to use their one-time, irrevocable chance to maintain status quo to not participate in the new MBCBP based largely on this fact.

I haven’t heard this drama first-hand. I left the angry widget pilot Facebook group a while ago (and my QOL has skyrocketed.) I don’t really care what Poor Old Joe does at this point, but before you listen to him, you should read about the loophole I just realized related to the mandatory nature of the MBCBP.

Frankly, I’m ashamed I didn’t latch on to this sooner.

Sorry for the clickbait-y title. I think this will make a big difference for a lot of pilots.

The Old 401k Horse Race

It used to be that any pilot wishing to maximize Roth 401k contributions had to “race” the company to fill up as much of their 401k with their own Roth contributions as possible. Each month, any money from the company’s 16% DC would (and could only) be deposited as Traditional 401k funds.

Some years, this led me to set my personal contributions at the maximum 75% allowed by Fidelity’s website. A senior Delta captain might have been able to reach the $66,000 total per year 401k contribution limit in February, especially if it was a good profit sharing year.

Then, about 18 months ago, Delta and Fidelity changed this policy to allow in-plan conversions for company contributions. (You may be able to read the details in MEC Alert 22-02.) This means that no matter who contributed the funds, the pilot or the company, those funds can all be converted into Roth 401k money.

This is a big deal! It’s easy and valuable for anyone who wants to maximize the Roth side of their account. (That may not necessarily include you. Talk with a CFP to find out whether it does.)

Note that the pilot will have to pay ordinary income tax on any funds converted from Traditional to Roth dollars. If that’s your goal, though, it’s worth it.

A pilot maximizing their own contributions to win the old horse race with the company would have ended up receiving a lot of 401k Excess (“spill cash”) for the rest of the year. I also didn’t mind this. It was like getting a 16% raise starting around March or April every year.

It turns out that we’ll be able to use a similar strategy to exercise significant control over how much money goes in to our MBCBP each year. Although it’s not full control, and it’s not a perfect solution, it’s enough control that it should tip the scales in favor of the MBCBP for many pilots.

Minimizing MBCBP Contributions

Let’s see what things look like if a pilot wants to minimize the dollars that the company puts into the MBCBP on their behalf this year. We’re going to use the MBCBP Calculator I built for this purpose. (Please, for the love of all this is good in this world, stop asking for permissions to view, comment, or edit this file. Just use “File -> Download” or “File -> Make a Copy” to get your own version.)

The key to making this happen is for our theoretical pilot to minimize their personal 401k contributions. Don’t worry about all of the other setup parameters in the calculator for now. Just make sure that the yellow box next to “Personal 401k (%)” is set to 0% like this:

For this exercise, we can ignore the middle part of this spreadsheet. (I even highlighted all those rows, right clicked, and selected “Hide Rows” to get them out of the way.) Here are this pilot’s results:

For this Year 8 B737 CA flying a lazy 72 hours per month, the only money that goes into their 401k for the year is the company’s 16% DC. This ends up being a total of $45,155 for the year. Note that since this is below the IRS limit of $66,000 (with some caveats we’ll discuss shortly) this pilot receives zero 401k Excess.

For a MBCBP participant, this would mean zero dollars were deposited into their MBCBP for that entire year.

This means that this pilot had full control over their MBCBP this year, despite having made a one-time, irrevocable decision to participate in the plan.

Think about the significance of that for a moment.

Maximizing MBCBP Contributions

Let’s say this pilot has an identical twin who loves tax-deferred dollars piling up in their MBCBP and wants as much money in it as possible. This twin pilot sets their “Personal 401k (%)” to the maximum 75%:

And here’s the result:

In this situation, the company only manages to get $11,289 into the twin’s 401k account. The twin maxes out their $22,500 annual IRS limit for regular 401k contributions and then uses the back-door (401A) option to put another $32,211 into their account.

(Note that the $32K 401A dollars are after-tax money, so our twin might as well convert them to Roth dollars. The $22.5K could be Traditional or Roth, but if this pilot is trying to maximize MBCBP funds, they’re probably trying to maximize tax deductions and would leave this portion as Traditional 401k. A Certified Financial Planner (CFP) can help you make that decision on a year-to-year basis.)

Since this twin hit the $66K per year IRS limit on their 401k in April, every other dollar of the company’s 16% DC for that year would go into the MBCBP. (In a year with good profit sharing, the twin would have probably hit the limit even sooner.)

Both pilots had the same overall compensation just over $327K. However, the second, maximizing twin put a total of $99,866 into tax-advantaged accounts while the minimizing pilot from earlier only put $45,155 into those types of accounts. The twin got an extra $54,711 in tax-advantaged income this year, and would pay a lot less in taxes.

What really matters though? Both pilots got exactly what they wanted.

The maximizing twin got the largest possible amount of tax-deferred income for the year, and reduced their tax bill. The minimizing twin prevented any money from going into the MBCBP, even though they’d made the irrevocable decision to participate in it.

The beauty of this is that each of these pilots has the power to continue changing their mind from year to year, even though they’re locked into the MBCBP.

Caveats

Let’s discuss two important caveats.

First, remember that pilots over age 50 get an extra $7,500 per year in their 401k, for a total annual contribution limit of $73,500. That could potentially allow a MBCBP participant to spend more years without putting money into the plan, if desired.

Second, there’s a limitation to this strategy that I haven’t addressed at all until now. In the convoluted bowels of the IRS code lies Section 401(a)(17). This section sets a maximum income limit for a person to receive company direct contributions for a 401k account. For 2023 this limit is $330,000.

Our contract addresses this limit, and after reaching $330K in total compensation for the year, we just get the rest as 401k Excess dollars. Starting in October, those dollars will go into the MBCBP for most pilots.

(I didn’t program the $330,000 compensation limit into my calculator. Apologies. That section was already complicated enough. Maybe I’ll get around to it at some point.)

This may require some manual calculations on your part. The key takeaway is that if you’re a MCBCP participant trying to use this loophole to minimize money going to that plan this year, the best you can do is 16% of $330K, or $52,800. Again, this loophole isn’t perfect, full control over the MBCBP, but it does allow participants to maintain a lot more control than I’d realized until a couple days ago.

For pilots who use my calculator and see that it doesn’t cumulatively make sense for them to start participating in the plan for a few years, this strategy could tilt that math in favor of participation now.

For pilots who want to look at the older decision point on my calculator from when we thought we’d be able to jump into and out of the plan from year to year, this strategy gives you most of that option back.

I hope this helps many pilots breathe a sigh of relief.

More Examples

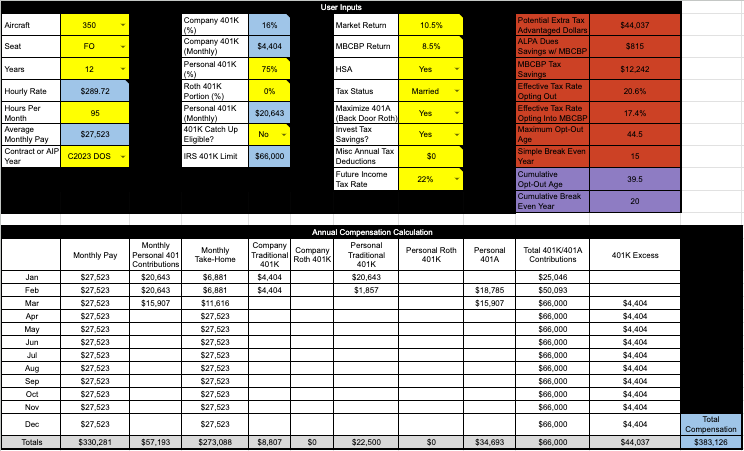

You should use my calculator to try out some scenarios. However, let’s consider a few here. First off, let’s consider a senior Delta widebody FO. At today’s pay rates, this pilot could fly an average of 95 hours per month without a single dollar going into their MBCBP.

If this pilot decided they wanted to instead maximize MBCBP contributions, their results might look like this:

This pilot would be able to get $44,037 into their MBCBP, protecting a total of more than $104,000 from taxes. (Of note, that’s how much money I made in my first year at my airline. Impressive.)

Since this is the highest FO pay rate on our charts, pilots in any other aircraft should be able to work even more hours while being able to prevent any of their compensation from going into the MBCBP in a given year. That’s a lot of control.

Let’s look at some possibilities on the Captain side too.

On the low end, it appears that a senior B717 CA participating in the MBCBP could credit an average of about 91 hours per month without a single dollar being deposited into that plan:

A Captain at the top narrowbody pay rate would be more limited, only able to credit an average of 78 hours per month if the goal was to keep money out of the MBCBP:

A harder working narrowbody captain would end up with some spill cash going into the MBCBP, but it wouldn’t be an extreme amount. At 100 hours of credit per month on average, this captain would end up with less than $15,000 contributed to their MBCBP for the year. (The calculator only shows $1,104, but remember the stupid IRS rule that caps 401k contributions at $330K of income. That would trigger for this pilot around September.)

Even if this doesn’t meet 100% of this pilot’s goals, it’s still a pretty good deal overall. This would end up with $67,104 in tax-advantaged dollars for the year, in addition to $419,000 of regular income.

If the MBCBP will be the right answer for this pilot at any point in the future, would it be worthwhile to reject that option forever based on an extra $15K going in to tax-advantaged accounts this year? I say no.

So What?

Some pilots seem to erroneously assert that choosing to participate in the MBCBP will lock away large portions of your income until retirement. That uneducated opinion could lead pilots to miss out on a great opportunity.

Most MBCBP participants will retain the ability to choose how much money gets contributed to our MBCBP each year, up to the IRS’s 401(a)(17) income limit of $330,000 per year. (Note that this limit increased $25,000 from the 2022 number. I suspect it’ll continue to rise, giving us increased maneuvering room over time. This is good because our pay rates also continue to increase, and the company’s DC rises to 18% by the end of our new contract.)

For pilots with incomes high enough to exceed that limit, the amount of spill cash that ends up in the MBCBP won’t be so much that it should ruin anyone’s short-term financial plans. I think that many pilots will be better off participating in the MBCBP, using this loophole to exercise significant control from year to year, and then using their time from now until age 59 1/2 to plan how they’ll put their MBCBP funds to use once they can roll them over to a (potentially self-directed) IRA.

That’s just one guy’s opinion though. Run the numbers for yourself. Then, go talk with a financial pro who can give you some authoritative advice. Then, let yourself ruminate on things for a while. The window for choosing to maintain status quo and not participate in the MBCBP doesn’t close until the end of July. You have some time to think things over before you make a decision.

Thanks for reading this far. I hope this helps your family meet your financial goals. Fly safe!

4 thoughts on “MBCBP Participants Get a $330K Control Loophole”