The United States, and perhaps even the whole world, finds itself in the midst of a pilot shortage. This is not debatable; this is fact.

You may choose to debate whether it’s a pilot pay shortage, or just a lack of qualified individuals. The bottom line though is that airlines are having trouble filling pilot seats on their jets.

Let’s be clear: this is morally wrong. It’s the worst human resources policy in our industry in recent memory. The geniuses who thought this up should get immediate performance reviews.

I suspect the Teamsters will find it relatively easy to fight this policy, and that it will go away quickly.

It doesn’t matter whether they succeed though. If you are a young pilot thinking about applying to a regional airline, you should avoid Republic Airways at all costs!

Even if this policy gets revoked, the fact that this company’s management was clueless enough to publish it in the first place should tell you everything you need to know about what it’s like to work there.

I think Republic will suffer a lot more than it already has from this policy. Remember that they’re the company who went bankrupt in 2016 specifically because they couldn’t staff their airline. It appears that they had no idea how to attract or retain talent back then, and they haven’t learned even after screwing over their shareholders and creditors. I’ll be surprised if this company continues to exist in the long term.

The Rock and the Hard Place

To the managers at all the other regional airlines: we all understand your position. You work at the mercy of bigger airlines. They compete you against each other and lock you into the least lucrative contracts possible. You have to honor those contracts flying the least efficient jets in the industry.

Your pilots have gotten nearly as expensive as their mainline counterparts. You have a terrible time retaining them. God’s honest truth is that any pilot who is qualified to work for you is qualified to work for better pay, flying better jets, under better work rules at a ULCC…if not a major like American, Delta, or United.

You’d probably love to hire some shiny, new, inexperienced pilots, but despite ALPA’s insistence, there aren’t enough of them to go around. (Part of the problem is that ALPA is counting a lot of pilots who have no intention of ever becoming airline pilots, but I digress….)

To have any hope of continuing to exist as a corporation, you must staff your aircraft and cover your flights. It will take incredible creativity and leadership (as opposed to management or administration, my esteemed MBAs) to achieve your objectives.

What follows are some suggestions on key points.

I don’t care if you like what I have to say or not. I’m just a random line pilot typing shit into a computer. My family has adequately filled our Treasure Bath and don’t even depend on my airline’s wholly-owned regionals for our subsistence. If you choose to give my thoughts consideration and try my suggestions, I think you have a chance of succeeding in this environment. If not, well, good luck.

What Are Our Assets?

When the Dread Pirate Roberts awoke from his mostly-death experience facing an enemy force twenty times the size of his own, this was one of his first questions. You should be asking yourselves the same thing.

My sources suggest that this is an actual photograph from the Republic Airways board meeting where their most recent pilot retention policy was approved. And you think a little head jiggle is supposed to make pilots happy, hmm?

However, before you get to assets, you should ask yourselves, “What are our weaknesses?”

You have two big ones, and they’re titanic:

Your Scope sucks

You have the worst work rules (and therefore pilot Quality of Life) in the industry

You can try to ignore these facts, but if you do you will fail.

So, what might you be able to count as assets? Here are a few things:

You can (and do) hire the least experienced pilots in the industry

Your relationships with major airlines present exclusive opportunities for flow-through programs

Your companies have always been short-stay locations for many pilots, and you’ve always been structured to deal with that as best you can.

And I’m spent. Sorry. If only we had a holocaust cloak….

The only solutions to your problems will have to address your weaknesses and capitalize (effectively) on your assets.

Simple Defense

Some of this should be easy. Your line pilots and their unions are probably suggesting everything I’m about to say and more. If you’d bother to listen, they’d essentially solve your problems for you.

Since your Scope sucks, you need to go out of your way to meet as many of your pilots’ needs as possible. On this front, realize that they:

Need as many total flight hours as possible, as soon as possible

Need to feed their families

Part of fixing this is getting your pilots their hours. I know, it’s tough to do this flying EMB145s or CRJ200s. A friend of mine used to complain that he’d work a 12 or 14 hour day flying 6 legs on the CRJ200, but he’d only log 2.5 hours because the legs were so short.

Sorry, but no pilot feels compelled to stick it out in that situation when they can go to Frontier and fly legs 2-3 times as long on a jet with 500% more flight deck floor space and a tray table. This means you need to tailor your trip mix to share the love on long legs. It also means you need to be lobbying your major airline masters, hard, to abandon inefficient 50-seat jets and at least fly the CRJ900 or EMB175.

I think you’ve largely figured out putting food on tables. Regional airline pay rates have skyrocketed lately. Until Delta’s recent contract, it was the Line Check Airmen at American’s wholly-owned subsidiaries who enjoyed the highest pay rates in the industry.

Your pay is fair. If it’s proving insufficient to attract and retain pilots, that means you’ve only just caught up to the industry standard on pay and now you’re lacking in other areas.

This goes back to your second major weakness: you treat your pilots terribly.

I’m a B737 Captain in NYC, which means I fly with new-hire FOs coming from every other airline in the industry. I love hearing about life at their past airlines, but I am constantly shocked at some of your policies. Your reserve rules are brutal. Your trip construction is overwhelming. Your scheduling practices are shady. Your commuter policies, if they exist at all, are insufficient. I could go on, but I’m sure you’ve been ignoring similar feedback for years.

I don’t care if you agree with me. I don’t care if you think I’m uninformed. Either you fix this, or you will go the way of the Republic.

You need to give your pilots enough days off to have a real life outside work. If they want to volunteer to do extra flying to get hours sooner, fine. However, if you’re at all forcing or cajoling that volunteerism, you will fail.

You need to give your pilots the ability to do the right thing. Give them schedules, reserve rules, and commuting policies that recognize reality.

You change your pilots’ bases so capriciously that they will not choose to move to a base just because you assigned them there. Make it easier for them to get to work, and give them policies that keep them whole when their honest and reasonable efforts to get to work fail.

These are just some simple basics. These are table stakes. If you want to succeed, you’ll have to start from here and think of even more ways to mitigate your weaknesses.

Yes, this will cost you money. Piedmont, PSA, and Envoy are paying LCAs $427/hr. You can afford to splurge a little on work rules.

Credible Offense

Now that we’ve covered the table stakes for addressing your weaknesses, let’s consider some opportunities for a creative airline to gain an edge on recruitment and retention.

Since you are capable of hiring, training, and employing the least experienced pilots in the industry, you should be out spreading that message with those pilots! You need to be at every industry conference, you need to be hosting get-togethers at aviation training hotspots and in major cities, you need to be buying chances to write sponsored content in trade publications, you need to on YouTube, TikTok, and Instagram showing how you take care of young pilots.

Many of you are doing this already. Good job; keep it up. However, the trick here is not to be like all the worthless influencers on social media these days who try to look cool, but don’t have any substance.

I can’t stand all the fitness gurus, home improvement “experts,” investing “pros,” “models,” etc. who try to pass themselves off as experts, yet provide nothing of actual value. (Hell, some schmuck airline pilots even have the temerity to blog about big-picture industry issues. I hope those chumps have some experience to back up what they’re saying!)

If you’re going to assert that you’re a great place for young pilots on social media, you need to make it true. Table stakes are mitigating your weaknesses, like we mentioned above.

Another part of this is not implementing policies that screw your people over. Republic’s most recent catastrophe is the perfect example. Another is Endeavor. Since Delta (wisely) relies on their wholly-owned regional to fill up larger jets at their hubs, they’ve made efforts to keep pilots at Endeavor for as long as possible…in fact they’ve tried too hard.

Though nobody will admit as much, it’s apparent that Delta is punishing any pilot who attempts to circumvent Endeavor’s flow agreement by applying directly to Delta or by going to another airline and applying for Delta from there. This is a terrible policy, and because of it I encourage pilots who want to fly for Delta to avoid Endeavor like the plague.

This is enough of a problem throughout our industry that I wrote a separate diatribe just on this topic. Only a great fool would go on social media purporting to be a good place for young pilots while implementing this type of policy.

The Professional Pilots of Tomorrow specialize in mentoring aviators. Any airline manager worth their stock options should be begging PPoT for some ideas on how to do better by their people.

Instead, you should have the world’s best mentoring program for new pilots. You should go beyond just basic airline career coaching and hire financial advisors, come up with job placement programs for spouses, and set up deals for affordable child care with credible providers, at least near your pilot domiciles.

You also need to put the right pilots into your training department. Some of you have a reputation for being too tough, and I promise you’re suffering for it. You can accept a reputation as, “tough, but fair,” but you need to publicize how you go out of your way to give every pilot a great shot at succeeding.

Like it or not, you also need to celebrate when your good pilots move on to bigger and better things.

We’ll get to how you can make these strategies win/win in a moment.

Before we go there, you also need to figure out how to make your flow-through programs non-punitive. If your program looks like a trap, pilots will assume that’s the case. You need more carrots here than sticks.

Part of that means getting better assurance of progression to your major airline partner. As I understand it, when a pilot interviews at Horizon, they are also interviewing at Alaska. There is no second interview. There is no “maybe.” Once a pilot has checked a clearly-defined set of boxes at Horizon, they move on to Alaska in one of the next two or three classes. Period, dot.

That’s the bare minimum industry standard for a half-decent flow through program.

If that’s not how yours looks, fix it. Does your major airline master dislike this fact? Ask them whether they want you to be able to staff yourself to cover their schedule or not. It’s that simple.

Mutual Benefit

Much to my chagrin, it appears that neither airline managers nor union bosses get sufficient training in logic or psychology. This is most evident in their inability to successfully win the Prisoner’s Dilemma in their pilot retention efforts.

Both sides act as though their only hope of success is screwing the other side over as hard and as often as possible. As a union member, I tend to believe that the management side has more than earned its distrust. However, labor relations at some companies have become so toxic that it’s too much for me to stomach.

Both sides in these battles must admit that there are mutually-beneficial solutions to all of these problems.

Airline managers should realize that their unions have probably been trying to explain these solutions for ages.

Union bosses need to get over the stigma of being in the company’s pocket and realize that it’s okay to work with the company for mutual-benefit.

Both sides need to sit down and work together in good faith to find ways forward. If I were king for a day I’d have the two groups sit together around a campfire with coolers full of chilled beverages and a table full of pizza nearby. Each side would spend as much time as necessary explaining what they think the other side’s pain points are.

There’d be no discussion, debate, or problem solving until both sides had said their piece.

If they accomplished that simple exercise, they’d realize they already understand each other, have some common ground, and that they both dislike some of the same things.

From there, a group of mature adults should be able to start figuring out ways to ensure reliability and flexibility for the company, while protecting pilot pay and QOL.

If I didn’t like my situation at my current airline so much, I’d think about branching out and starting my own airline based on this philosophy. I’m confident that I could come up with a more efficient and reliable system while attracting and retaining pilots that would be so happy we’d cause huge problems for the rest of the industry.

I honestly hope someone else gives this a try. If you do, you’ll be the one that all the other CEOs and union leaders envy.

Or you could just be the next company to “pull a Republic.”

(Nope, it’s not too soon. They made that phrase part of our industry’s lexicon all in one day!)

Ultimate Solution

Like it or not, these are only stopgap measures. Regional airlines should never have existed in the first place.

These atrocities only came into being in the wake of crooks like Frank Lorenzo who raped and pillaged our industry by ruining good companies and the lives of the families who built them.

They demonstrated that some pilots could be desperate enough to work for less pay and under bad contracts based on the promise of something better down the line. That, combined with the introduction of smaller passenger jets that never lived up to their promises, prompted major airline execs to form regional airlines. These shitty shadows of their major airline masters were places where execs could bank losses, pay pilots peanuts, and treat both customers and employees like garbage.

I say again: Regional airlines should never have existed in the first place.

That knowledge presents the obvious solution: get rid of regional airlines.

There is truly no point to a wholly-owned regional today. Regional pilot pay rates offer no savings. You’re forced to duplicate your corporate structure, including very highly-paid management and executive positions. Worst of all, you’re operating the least efficient jets in the industry.

I flew the A220 for a couple years, and it is a masterpiece! It should replace every regional jet owned by a major airline. The A220 has roughly the same hourly fuel burn as a CRJ900 or EMB175, yet it carries 30-50 more passengers!

Not only that, the A220 has the best narrowbody cabin in the industry. It has real overhead bins and real cargo bins. It can efficiently cover regional jet routes, but it’s also capable of flying a US transcon with an alternate. Bombardier even flew one from London City Airport to NYC, westbound, in the winter!

As much as I love the A220, it appears that the A321neo and B737MAX are even more efficient. While I’d rather see more A220s in the skies, you can probably increase your profits and pax ex by using some flavor of re-engined Airbus or Boeing product to replace your 76-seat regional jets in many of your markets.

No matter what aircraft you choose, there is no excuse for you to be operating worse, less efficient aircraft at wholly-owned subsidiaries. Even if you hated your pilots, you have a fiduciary duty to your shareholders to make the right decision here.

Will there always be a need for the smallest jets in the industry to serve the smallest markets? Yes.

That’s what independent companies like SkyWest are for. Hire them to provide feed between your smallest markets and your hubs. Let them specialize in that. If they want to waste money, they can do it in 50-seat jets. Or, they can fly 76 seaters on those routes while you fly 110-130 seat A220s on routes that your wholly-owned 76-seat jets used to fly.

If you want, you’re welcome to keep some of your 76 seaters as mainline aircraft.

I’ll probably commute for my entire career. If I had the option of driving to work to fly a mainline EMB175, I would absolutely consider volunteering. You’d probably find a lot of pilots like me. You wouldn’t need them though, because all those pilots from your wholly-owned regional would now be available to fly those jets as mainline pilots.

That is the ultimate answer to designing a better flow-through program and not trapping pilots in it. Don’t make it a flow-through. Make all your pilots mainline. The junior ones will get stuck flying junior jets at junior bases. You’ll have a better spread of experienced pilots to fly with them. You’ll eliminate your expensive and wasteful redundant corporate structures. You’ll give your passengers a better and more consistent experience.

This is not a win/lose strategy. This provides wins for everyone.

The first airline to figure this out will change our industry (for the better) forever. They’ll also get a huge lead on pilot attraction and retention. I hope it’s mine, but if not, I hope it’s yours.

Onward

This is Part 1 in a series that will address pilot retention at various levels in our industry. As it turns out, the stakeholders at all of those levels have good options for winning, if they’re willing to exercise some conscious thought and try something new. We’ll tie everything up by showing how working together across existing divisions would take win/win philosophy to a whole new level for everyone.

Until Delta’s recent contract, regional airlines were offering the highest first-year pay rates in the industry. Regionals have stopped hiring FOs because, even after forcing hundreds of pilots to upgrade to Captain against their will, they still don’t have enough left seaters.

This is happening because major airlines need every pilot they can get to staff operations that are simultaneously recovering from COVID and growing overall, just a year or two after they allowed thousands of pilots to retire early during the pandemic. The only reason this won’t be the busiest major airline summer in history is that there aren’t enough Air Traffic Controllers in the country to handle the volume of traffic our companies want to throw at them. That only means demand will continue to climb, unsatisfied, until the FAA can get its act together and get more controllers hired and trained.

On top of this, America’s ULCCs are also expanding and hiring like crazy. They’ll hire a regional pilot and get them more hours, more efficiently, in a better aircraft, while working under better work rules, but only if the major airlines don’t snag those same regional FOs first.

Don’t forget that demand for large freight has only increased over time. Amazon is continuously expanding their operations, and other carriers are struggling to keep up. (FedEx is trying to make it look like their demand is dropping. I believe that much of this is shenanigans, driven by Purple management’s stance in their ongoing contract negotiations. Unfortunately for them, Amazon and others are more than happy to scoop up all the market share that FedEx is giving up. Soon, cargo formerly flown by a FDX B777 will be carried on a Hawaiian A330.)

This mayhem gives young pilots a lot of choices, which is both good and bad. I constantly hear questions from pilots trying to figure out the fastest way to the majors. They include:

“Should I upgrade at my regional, or jump to an ULCC?”

“Should I upgrade at my regional, or fly widebody jets at an ACMI?”

“My ULCC seems to have good pay and work rules. Should I really leave for a major airline?”

Amidst that discussion, I also hear some really terrible advice and opinions that lack any semblance of context or consideration. Common refrains include:

“I’m happy where I am. I’m senior and have the best schedule of my career. Why would I go elsewhere to start over as a junior FO?”

“ULCCs are major airlines.”

(It strikes me as ironic that many of the loudest voices behind this one are people who have since ditched their ULCC for an actual major.)

“I make as much as a Delta Captain here.”

“I can’t afford the pay cut.”

Just this morning I read a post from a NetJets pilot who likes his job and can hold an upgrade at 18 months in. He has a CJO at Delta, but is thinking about foregoing it because he’s worried about being on reserve for a few months and possibly missing out on holidays for the next year or two. (I know, I can’t make this stuff up.)

Here’s the bottom line: you owe it to yourself and your family to pursue a job at a major airline. By “major” I mean one of:

American

Delta

FedEx

Southwest

United

UPS

Why? I could spend all day giving you reasons, but I hope to center my points here around a single area: Scope. It turns out that Scope is the single most important factor in every airline pilot’s career.

What is Scope?

When I left the Air Force for the airlines, I had never heard of or considered Scope. Someone explained it to me, and it made sense, and then I voted on our 2016 contract without any consideration for it.

Wow Emet, you were a moron.

Yes I was, but in the words of the guy who got turned into a newt: “I got better.”

Scope is the term for expressing what flying your airline does. It encompasses the types of aircraft, where they fly, and who flies them.

Scope is Section 1 in my pilot contract for a good reason. It is the most important job protection I have. Our scope section states that our company can only fly jets with our livery. Those jets must be flown by two or more (and never just one) pilots on the company seniority list.

We recently signed a new Global Scope agreement with our company that offers us even more protection. Here’s a great podcast episode with details:

This Episode of the Engage Podcast explains the enormous gains the Delta pilots achieved with their new Global Scope agreement. If you care at all about the future of your career, you need to be screaming for your union to negotiate similar protections.

Our company has spent the last decade or so entering Joint Venture (JV) agreements with foreign airlines. They’re like codeshares, but deeper. Until recently, they allowed the company to outsource our jobs to foreign carriers. This was bad. Our new agreement forces the company to reset the balance of flying for which it uses JV partners, and put more of our pilots on our widebody jets for long-haul flying. This is the most important thing that has happened for my pilot group since bankruptcy and mergers in the mid-2000s.

Scope Problems

Although the majors are slow to admit it, they currently depend on regional airlines for their very existence. Delta Air Lines makes 2/3 of their profits each year from domestic operations. Until COVID, this meant $4B of their $6B profit every year came from domestic flying. The only way to make that happen is to have small RJs feeding thousands of passengers into and out of Delta hubs every few hours.

United Airlines has lots of gorgeous B777-300ERs and B787s. It’s relatively easy to get to the right seat of one of those wonderful widebodies. Rumor has it that Captain seats are even going unfilled on those jets.

These aircraft fly to lots of desirable international destinations. However, United has a huge low-end Scope problem. In a good year, United only makes about half as much profit as Delta, total. If you look at market cap, United is only worth about half as much as Delta, despite having more, newer widebody jets. (This post has some numbers to back these claims up. They’re older, 2018 numbers, but I suspect they’ll continue to hold true for the near future.)

What’s the difference? While United was spending all that money on shiny new widebodies (that it had to compete unprofitably with against the ME3 and shitty airlines like Norwegian), it completely neglected the regional end of its operation. Now, they’re having trouble filling those big jets because they just can’t connect passengers from small-town America to their big hubs.

The Scope clause in the United pilot’s contract places significant restrictions on the number of regional jets their company can operate. United’s managers are begging their pilots to modify that scope clause and let them improve their regional feed.

I believe the pilots have taken exactly the right stance: they’ve stood firm and said, “Hell no!”

At the same time, they’ve offered solutions. Essentially, the United pilots told the company it can have as many small jets as it wants, as long as it makes them mainline jets flown by mainline pilots. (Here’s a short summary of this fight.) If I were a United pilot, I’d love to be a CRJ900 or ERJ175 Captain, flying at mainline pay rates…especially if they decided to add more pilot bases in places like TPA or MCO to ensure they had enough ramp space.

Better yet: United could buy the stellar A220. It has the same hourly fuel burn as a CRJ900 or ERJ175, yet carries 30-50 more passengers, has the best narrowbody cabin in the industry, has actual overhead bins and cargo compartments, and has enough range to for transcon flying with an alternate, or even flying across the Atlantic.

In classic airline management style, United’s CEO told his pilots to pound sand. Instead, he went to the trouble of getting FAA certification for a completely new aircraft type, a CRJ700 with only 50 seats onboard, called the CRJ550. This gave United’s managers the leeway to accomplish some of their goals without having to renegotiate Scope with their pilots.

This appears to have been somewhat effective in the short term. The United pilots are smart to try and get more of that flying at mainline. However, until management caves, United is missing out on billions of dollars in potential income. This is bad for their shareholders, bad for the long-term health of the company, and it means United’s pilots may never enjoy the incredible profit sharing payouts that Delta pilots have traditionally enjoyed.

(If only United’s shareholders were to hold United’s executives accountable for this painfully obvious neglect of their fiduciary duties….)

Regional Scope Will Always Suck

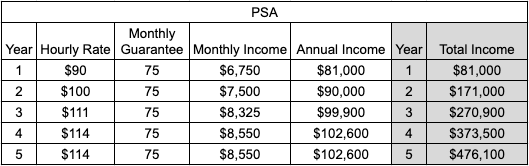

Regional pilots must realize that your Scope sucks. Most regionals in the US only work for other carriers. Their customers don’t know the difference between Republic, GoJet, PSA, or SkyWest, if they even realize those companies exist at all. If your company’s name isn’t painted on your jet, you have a Scope problem.

The solution here isn’t to make regional airlines bigger, or to get more recognition for those companies. The sad truth is that CRJ and ERJ aircraft aren’t efficient enough to make a profitable nationwide airline. If a pilot wants better Scope, the only option is to move up to a better company.

Quality of Life

Since most regionals are at the mercy of larger airlines, they are under intense pressure to perform, but also have the lowest priority.

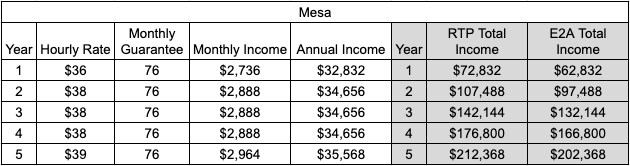

Imagine the pressure that United puts on Mesa to complete each and every flight. They’re so desperate for regional feed that they created the CRJ550. This forces regionals like Mesa to do whatever they can to attract pilots.

Once they have a pilot on the line, they need him or her to fly several legs a day, just to break even. They can’t afford to give pilots more than 10-12 days off per month, and they’re definitely going to use every single reserve pilot, every day.

I’ve heard countless horror stories of regional pilots answering phone calls only to hear, “Come in to work immediately, or else.” One pilot was on a beach, on assigned vacation days, and told she had a choice between coming in to work or being fired.

This is utter bullshit, and yet that is how regional airlines operate.

Regional pilots, please understand that this is not okay. One of the many reasons you need to move on to a better company is that contracts at good airlines protect you from this kind of garbage.

At my major airline, I’m almost never obligated to answer the phone, period. If I happen to answer a call for an IA, I still have lots of protections. I average working 8-14 days per month…probably about the same number of days you have off. My schedulers can’t even reach me, let alone force me to come in to work. You deserve to live under this kind of contract.

This is just one example out of hundreds where pilot contracts at regional airlines have terrible work rules, compared to major airlines. If you stay at a regional, you’re accepting worse Quality of Life than you should have to.

What is This? Career Progression for Ants!?

So, regional airlines pay the worst, and treat their pilots the worst. It doesn’t stop there though! Staying at the regionals means you’ll suffer from that bad QOL for the longest amount of time possible.

I didn’t even realize this until my friend J-Lo spent a few years at Endeavor.

He had enough hours for an ATP, but really needed a quick 1000 turbine hours, and ideally as much turbine PIC as possible, to be competitive for a major. He did the right thing and upgraded ASAP to start logging those PIC hours. Unfortunately, this meant flying the CRJ200…the worst jet in our industry.

One of the many problems with the -200 is the fact that it has short legs and is load limited. While it’s theoretically capable of longer flights, it’s most useful (if useful at all) on very short legs to and from hubs. J-Lo flew many 6-leg days without leaving the state of Georgia. Some days he’d never even touch FL180.

The biggest problem with these short legs is that they happen quickly. A flight between ATL and CSG averages less than 20 minutes. This meant that even after a back-breaking 6-leg day, he might have only logged 2.5 total block hours. Sure, he had a 4-hour average daily pay guarantee, but that doesn’t get you to a major airline sooner.

Compare that to operating an A320 or B737 family aircraft for a ULCC or major. Sure, those aircraft do some short legs just like J-Lo’s CRJ200…especially at certain airlines. However, those jets are also capable of 6- or 7-hour flights. A pilot on one of those fleets stands a much better chance of logging 4-8 flight hours per day for 1-3 legs of flying, rather than 2.5 hours for 6 legs.

It doesn’t take much Pilot Math to realize how much faster flying for a ULCC will get you the hours you need to be competitive at the majors.

While pay rates at regional airlines have recently risen to match those at some ULCCs, they’ll also be the first companies to slash pay rates when times get tough. Also, it’s a lot more efficient to get paid 4-8 hours of pay per workday at a ULCC than crediting up to your 4-hour ADG at a regional.

At this point, you may be wondering why someone would ever fly for a regional. In a way, so am I.

On one hand, many regionals offer flow-through programs to major airlines. Those programs sound good on paper, until you realize that they weren’t instituted for your benefit. They are 100% traps designed to protect regional staffing and low-end scope for major airlines.

The reality of our industry right now is: if you’re senior enough at a regional to be close to getting a flow-through date, you’re competitive for every single major airline. For this reason, I strongly advise pilots to NEVER fly for a regional with flow through to your #1 major airline. This could block you from applying off the street and cost you years. Pick a regional with flow to one of your 3rd or 4th backup companies. Worst case, you can use that program, but only if the company you actually want rejects you.

Another reason to go with a specific regional might be the commute. All else being equal, you’re better off not commuting. If you can live in base at a regional, and get the flying you need, that might be an okay option. However, don’t let getting cozy in that situation prevent you from moving on when the time comes. (More on that shortly.)

Another reason many pilots consider regionals is that they’ll take inexperienced pilots and pay for the ATP CTP course. Some airlines even offer time-building programs, in exchange for indentured servitude in the future.

I get it: when you’re new, money is tight. The idea of getting that stuff covered is attractive. However, if that’s the only thing holding you back, go get another loan! Going to a regional for that reason alone is penny wise and pound foolish.

If taking a handout now slows down your career progression, you’re not missing out on a few months of ULCC new-hire pay. You’re missing out on top-line A350 or B777 Captain pay at a major. Delta’s new contract puts that at $474/hr, easily over $500K per year. Don’t give up months or years of that pay to get a free $5K CTP course or $30K in Seminole hours now.

Major airline FO pay is so high right now that you can rapidly pay off any loans you need to. Yes, this advice is coming from the guy who wrote Pilot Math Treasure Bath and says that debt is a bad thing. In this case, it’s an investment, and the long-term rewards are worth the near-term pain.

So…ULCCs for the Win?

So, if regional QOL is so bad, the ULCCs are just as desperate for pilots, and those ULCCs have essentially the same hiring minimus as those regionals, why not just go fly for a ULCC instead?

In general, I think this mentality is right on.

The ULCCs pay either the same as the regionals, or better. However, you’re likely to log more hours per workday meaning fewer days per month at work, you accrue flight hours more quickly, or both. The work rules at the ULCCs also tend to be much better than those at the regionals.

These are a few ULCCs where I believe most pilots could happily enjoy a full career. You’re much better off getting stuck at one of them than at a regional. So, who are these carriers?

When it comes to Scope, there are several carriers operating A320s, B737s, or even bigger aircraft that didn’t make my list of majors. I think of these as Tier 2 airlines. They include (but are not limited to):

Allegiant

Spirit

JetBlue

Frontier

Breeze

Sun Country

Avello

iAero

There are also several Tier 2 cargo carriers including:

Atlas

Kalitta

ATI

Amerijet

Western Global

Alaska and Hawaiian will tell you they don’t fit in this tier…that they’re “majors” or “legacies.” For me, Scope defines everything here.

In my mind, a major airline is one that owns widebody aircraft and uses them to do international flying to all 6 traditionally-inhabited continents.

(Yes, Southwest doesn’t do that. However, they’re a very large operation and they do a credible amount of international flying within this hemisphere. Yes, Hawaiian does more international flying than Southwest, using A330s and soon B787s, but they’re a comparatively tiny company and that flying is limited to a few destinations. These dividing lines aren’t perfect. I think Hawaiian is a good company, and it’d be awesome to live and fly there. However, they’ll never be able to compete with the QOL available at a true major.)

It isn’t just the flying at these companies though, it’s the work rules.

If you talk to pilots at any of these Tier 2 companies, you’ll hear lots of little complaints about things that seem small, unless you’ve had to deal with them in real life. You’ll hear about scheduling practices, pay protection (or the lack thereof), trip construction, sick rules, vacation policies, reserve rules, disciplinary policies, and more.

I hear about these issues on every trip I fly, because as a NYC B737 Captain I fly with new-hire FOs from all those companies all the time.

Most pilots find ways to exist successfully under these bad or mediocre work rules, but it’s always a struggle. The reason major airlines are so much better than the regionals and these Tier 2s is that our pilot contracts give us much better protection.

We have the best scheduling rules. They guarantee us the most days off per month of any pilots in the industry. They protect our pay, no matter what shenanigans scheduling pulls. They protect us from punishment. They offer us the best possible protection from unscheduled flying. Delta’s new contract locks much of that down by making it extremely expensive for the company to screw with us. Either they’ll have to build better trips, or we’ll get even richer than we already are.

Choice

Another important aspect of the whole Scope dynamic boils down to one thing: choice.

Southwest is a great company that pays well and has a good contract. However, if you work there the only aircraft you will ever fly for the rest of your career is the B737. (Unless they suck it up and buy B787s. I hope they never do, because they’d be a powerhouse and I would hate to have to compete against them!)

Southwest works their people hard, frequently flying numerous legs per day, and that can get exhausting when you’re stuck flying what is arguably the oldest and worst mainline jet in the industry. Since there’s only one type of jet and only two seats on each, Southwest has a huge stagnation problem. If you want to upgrade, you’ll be waiting for years. When you finally do, there isn’t a great answer to “What’s next?” You’re going to be doing the same thing on the same jets…until you retire.

This rings true at a ULCC, except your pay and work rules will never be as good as what Southwest pilots get.

One of the reasons my primary definition for the majors includes widebody jets is that it means there is more career progression for everyone, more choice.

At the other majors, there is progression from narrowbody FO to narrowbody CA…or widebody FO if you want. Some widebody FOs will upgrade on narrowbodies, while others will just stay in their seat and enjoy the stellar QOL their seniority brings until they can be senior in the left seat of their same widebody jet. More recently, Delta has awarded new-hire FO spots on every jet in its fleet…to include the A330 and A350.

At major airlines, reserve goes senior among widebody FOs. There are fewer departures per day and those trips are worth a lot of money. Pilots are significantly less likely to call in sick and miss an international trip, so reserve pilots rarely get used. I’ve met more than one widebody FO who works an average of 5 days per month while earning 75+ hours of pay. I challenge you to show me anything at Southwest or a ULCC that can match that combination of pay and quality of life.

Don’t like what you’re doing? Feel like you’re stagnating in your current position? Just interested in trying something new? You’re never more than a 2-year seat lock from choosing to try something completely different in your life at one of these majors.

This aspect alone is a powerful QOL enhancer.

With all these choices, you also see plenty of movement at a major airline. Eventually, most senior FOs will upgrade to CA, and most narrowbody pilots will move on to widebodies. When they move, their seats go to more junior pilots. As Delta expands its fleet and pilot group, this situation has only gotten better. The junior Delta B757/767 (“7ER”) Captain in NYC got awarded his spot after 2.5 months with the company.

When Delta starts having to answer the mail on the new Global Scope agreement it signed with its pilots, it will be forced to immediately offer dozens or potentially even hundreds of new widebody spots. This only means more choice for everyone, more pilots at the top of our pay charts, and more opportunities for junior pilots to advance to positions years ahead of their peers.

You will never get these kinds of choices or opportunities at a company with lesser Scope. There aren’t enough aircraft types, there aren’t enough pilots, and there isn’t enough long-haul international flying.

Sweet Little Lies

With this perspective in mind, let’s look at some of the stupid lies that many pilots in this industry tell themselves or each other.

I’ve heard:

“My ULCC seems to have good pay and work rules. Should I really leave for a major airline?”

Or

“I’m happy where I am. I’m senior and have the best schedule of my career. Why would I go elsewhere to start over as a junior FO?”

This should be clear by now, but the answer is a resounding, “DUH!”

The pilot contracts at major airlines are better than those at Tier 2 companies, period. They offer better protections and more money. I’ll ask you a version of the question I ask military pilots who are too institutionalized to leave:

“What do you love about flying at your ULCC that you can’t also get at a major?”

Do you like your jet? You can fly the same thing at a major airline.

Do you like your schedule? I guarantee you can get the same thing, or better at a major. Yes, if you only fly day turns at Allegiant it will take some time to get senior enough to achieve this at a major. However, it can be done.

Do you like your upgrade times? I’m not sure what beats unfilled Captain seats at United, and 2.5 month widebody upgrades at Delta.

Do you like your seniority? I get it. Even I’m guilty of indoctrinating you on the idea that Seniority is Everything. However, I promise you that even the most junior FO at a major has better pay and QOL than many of the most senior pilots anywhere else. I know this because I hear it from every single new-hire FO I fly with.

I regularly fly with FOs who have never sat a day of reserve at our company because they were already senior enough to hold a line by the time they finished OE. Worst case, they might be on reserve for a few months. Among NYC B737 FOs at my company, a year with the company puts you around 25% seniority.

For now, the argument that you’re giving up seniority moving from a ULCC to a major is shortsighted at best, and lazy or ignorant at worst. You’ll regain equivalent seniority in no time.

In a way, this won’t hold true for ever. The major airlines are on a hiring tear unlike anything in human history. Aircraft orders are through the roof, travel demand is insatiable, and every company is trying to expand. Every company is snapping up pilots as fast as it can.

However, there will be a point where pilot groups get a little too big. The airlines will reach a point of having enough pilots for the aircraft on hand. At that point, hiring will drop from 2000-2500 pilots per year per company to just enough to replace retirements, somewhere around 400-800 pilots per year, steady-state.

If you wait too long to move on from a regional or Tier 2 to a major, you’ll be on the wrong side of that wave and it’ll cost your family millions of dollars and untold QOL. If you value your time or money, moving over ASAP is your best option.

I cannot stand hearing:

“ULCCs are major airlines.”

They simply aren’t.

This doesn’t mean they’re bad companies! I frequently commute to NYC on JetBlue. I think they’re a great company with a lot of potential. If their merger with Spirit gets past regulators, and they abandon Spirit culture wholesale to just make JetBlue bigger, they’ll be a serious contender that should have Southwest worried.

I listened to Allegiant’s presentation at TPNx last weekend, and was very impressed. If you live in one of their bases, the idea of making great pay to be home every night is extremely compelling. I honestly would not fault a pilot for choosing that.

And yet, those companies aren’t major airlines. They don’t have the widebodies, the top-end pay, the long-haul international flying, the fantastic work rules, or the career options available at the majors.

I’ve found that the people who try to make this assertion are usually trying to push pilots into a deal that benefits their business more than it benefits the individual pilots, or they’re making excuses for their own laziness and stagnation. Don’t listen to it.

I’m especially frustrated when I hear:

“I make as much as a Delta Captain here.”

The problem with this statement is it completely lacks context. Can a pilot make that much money as a Line Check Airman at one of American’s wholly-owned regional airlines or as a Captain at a Tier 2 airline right now?

Yes.

However, to do it, that pilot has to work like crazy.

They probably live on their phone, shopping Open Time. They have to take short-notice trips that constantly detonate their family’s schedule. Many of them are flying so many days per month that they make 20-workday-per-month military pilots on the government gravy train look like homebodies.

Looking at my schedule so far this year, the most I’ve worked in a month was 15 days. With our new contract, I’m likely to work either fewer days per month or enjoy $5K+ in increased monthly compensation for zero additional work because our new soft pay rules are so powerful.

Some regional and ULCC pilots may make as much money as I do, but there’s no way they’re working as little as I do.

I’m a “less work for less money” kind of guy overall, but my phone rings off the hook with premium trips. If I spent as many days at work flying those Green Slips as the regional and Tier 2 pilots making these claims, I could easily make $50-60K per month, if not more.

The pay and contract rules at the majors are just so much better that regional and Tier 2 pay and QOL will never measure up.

Of all the bone-headed lies that airline pilots tell themselves, perhaps the most egregious is:

“I can’t afford the pay cut.”

When I started at my major airline, I made $104,000 in my first year (that’s in 2016 dollars). We’ve gotten pay raises in two new contracts since then. The latest one includes all those great soft pay rules, on top of industry-leading new-hire pay rates.

Yes, regional and Tier 2 pay rates have climbed astronomically above the $200/hr mark. Yes, this means jumping from one of those companies to a major might reduce a senior regional or ULCC Captain’s pay from $200K-250K per year to a measly $150K per year. Yes, that’s a big cut.

There are some serious problems with this mentality though.

First, what the hell are you wasting your money on if you spend every dime of your $250K salary every year? Only a supreme fool would spend so thoughtlessly. You will be the Poor Old Joe of your generation.

I went to great effort writing my book to prove that the average American family can live very happily on about $57K per year. I’m working on an updated second edition, and it looks like that number could climb to as much as $68K per year thanks to inflation. However, that’s a far cry from $250K. In my book, I even allow for arbitrarily doubling your spending when you upgrade to Captain, and that still only accounts for about half of what you’re making.

If the vast majority of Americans can live happy lives at a quarter of your current salary, the idea that you couldn’t be happy taking a temporary 40% pay cut is absurd.

If you’re spending every dime you make, then you need serious financial help. Hit me up and I’ll send you free copies of both Pilot Math Treasure Bath and Dave Ramsey’s The Total Money Makeover. Yes, I’m dead serious about that.

It could be that someone in your family has serious, chronic health issues that soak up all of your earnings. If that’s the case, you have my deepest sympathy. I think I could probably help you find a way to make moving to a major work.

However, I think this is not the case for the vast majority of airline pilots. If you’re spending everything you earn, you are setting yourself up for a lifetime of financial slavery. What you can’t afford is not changing your ways! I promise you can survive a year or two of reduced pay simply by changing your spending habits from “abject insanity” to “ever so slightly less opulent.”

Don’t act like this is a valid reason for staying at a regional or a Tier 2 airline though.

The second problem with this mentality is its malignant near-sightedness. Yes, even with Delta’s new pay rates, your first year at a major airline will be less than a top-line regional or Tier 2 Captain. However, if you look at Year 2 or 3 pay at Delta and UPS, you’ll see that you’re back to break even in a very short amount of time. (The other majors will have to match these rates soon, or they’ll have no hope of staffing their airlines.)

That doesn’t account for premium pay. I frequently fly with Year 2 FOs who are on their 3rd or 5th or 7th Green Slip of the month. This means they have spent several days each month flying for equivalent pay rates even higher than mine…above and beyond the flying they do for single pay! These pilots are making so much money, it’s just silly. Yes, it takes a lot of extra work. However, if finances are your only reason for not jumping to a major, you could probably break even just by picking up premium trips.

Also, don’t forget that upgrade times at the majors are shockingly short right now. It’s very possible to upgrade during your first year at a major airline, hitting pay rates that meet or exceed your regional or Tier 2 Captain pay while your indoc classmates are still on probation.

If major airline rates represent a pay cut at all, the time frame during which that’s true is so vanishingly short that it completely invalidates your assertion that you can’t afford it.

The final problem with this mentality is the long-term costs to your family.

All airline pilots eventually age-out. There’s talk that this age might rise to 67, but many pilots leave before 65 right now anyway. It is critical for you to understand that when you give up years at a major airline, you can’t think of those years at new-hire FO pay. You must think of those as years you could have been flying as a widebody Captain. Delta has set the industry standard for that rate at $474/hr, and it will only go up from there.

When you ignorantly say you can’t afford to take the pay cut, you assertion is based on a pay cut as high as $100,000 in your first year. However, you must realize that what your family is actually missing out on is a year of earning $500,000 or more. This means you’re giving up on an extra $250,000 – $300,00 in the future, not decrease of $100,000 now.

Before you stick to your guns on that one, go ask your spouse or significant other how they feel about it.

I know some of you will say that the Net Present Value of $100K today far exceeds that $300,000 in 10 or 20 or 30 years. While this is mathematically true, it’s only a valid argument if you’re actually investing that money.

In my experience, most pilots making this argument aren’t doing so because they’re only spending $68K per year and investing every other penny. They’re saying it because they’re spending upwards of $250K per year and investing almost nothing.

In that case, taking a pay cut for a year is the biggest possible blessing you could ever get.

This very temporary pay reduction could force your family to take a long, hard look at your finances. If that led you to make long-term spending cuts and/or investing increases, it would benefit you far more than even winning the lottery. Hundreds of lottery winners, professional athletes, and rock stars end up destitute because they never learned to spend intelligently. Unless you can get that figured out, no amount of airline pay will help you build actual wealth.

Take the pay cut. Fix your family’s finances. Learn how to fill up a Treasure Bath. In the meantime, you’ll be accruing seniority at one of the highest-paying airlines in the world and enjoying industry-leading QOL.

Do not scam your family out of these long-term benefits by asserting that you can’t give up a piddly $100k next year.

One Caution: American

Although I’ve made a lot of broad statements about the Big 6 major airlines, they are not all created equally.

The sad truth is that American Airlines’ pilots are in a tough spot right now. Although I’m not particularly impressed by any airline exec, American’s pilots have been stuck with some particularly toxic managers for far too long. These managers have made what I consider to be the terrible decision to try and compete at the low-cost end of the airline spectrum. I frequently sum up my perception of Doug Parker’s business strategy as:

“Let’s try to be Spirit Airlines, but with widebodies.”

It doesn’t take an MBA, C-suite credentials, or a decade plus of watching American’s decline to know that this is a stupid idea. Airline margins can be tight as it is. You simply cannot make more money by charging less for a worse experience. So many terrible long-haul ULCCs have gone bankrupt over the years, that it should be obvious how terrible an idea it is. And yet, that’s exactly where American has been heading for a while.

They’ve repeatedly been roasted by travel bloggers for shrinking seats, taking seatback entertainment screens out of their aircraft (because they actually thought passengers wanted that!), shrinking the size of their lavatories, and more.

Intertwined with the fact that American is drowning debt and not making as much money as their peers because they’re marketing a worse product to the lowest paying customers in the industry, is the fact that their managers have gone out of their way to stick their pilots with the worst contract among their peers.

American pilots have some truly egregious work rules, compared to industry standard, let alone new industry-leading provisions at Delta. Their pay now also lags their peers.

If you read or listen to Flying the Line, you might suspect the author blames this in part on the American pilots abandoning ALPA and getting stuck with a union that is way too closely tied to their company. (I get the feeling that anyone holding grudges is on their way out, and America’s pilots would be welcomed back into ALPA with open arms. Wouldn’t that be a coup for our entire industry?)

No matter why the American pilots are in this position, they have the longest way to go in the current round of contract negotiations. To their credit, they just completed a Strike Authorization Vote with overwhelming support similar to the results at Alaska and Delta that led to improved negotiations and new contracts.

I sincerely hope that the American pilots will prevail in their negotiations and achieve the contract that they deserve. I similarly hope that their execs will come to their senses on business strategy so that my friends there can enjoy working at a better company. I say this knowing it’d mean more competition for me, and that’s okay. Competition makes us all better, and I live in fear of my company getting lazy!

This said, until and unless American’s pilot group gets a better contract, I personally don’t believe it’s the best company for most pilots. I think part of what it will take to improve things at American will be for us as pilots to avoid that company like the plague. They need to feel the worst of the ongoing pilot shortage before they’ll be willing to make the improvements their pilots, customers, and other workers deserve.

This means that if you’re at a regional or Tier 2 airline (or American itself,) I can really only recommend applying to 5 of the US major airlines.

That said, I also hesitate to recommend Southwest based on the arguments I’ve made here. I lump them in with the majors because they’re a big company with a good culture, their pay is competitive with their 5 peers, and they have a very good contract. However, I couldn’t bring myself to do nothing but long days flying only the B737 around North America for the next 22 years. I need more variety in my life. I couldn’t handle that kind of stagnation.

I also worry that some of what makes Southwest special is eroding with time. They still throw the concept of “LUV” around like an Air Force Wing Commander promoting *Synegry*, but evidence shows that things may not be as LUVley there as they used to. Also, Southwest’s pilots love their archaic line-bidding process in part because it lets them scam 5 months of getting full pay for almost no work with just 5 weeks of officially awarded vacation. I worry that at some point their management (or their shareholders) will say “enough is enough” and that their good deal will go the way of the dodo…just like it did at every other major airline.

Overall, Southwest is still a good company for the right person in the right circumstances, but most of the arguments I’ve made here against Tier 2 airlines apply to them as well. Like I asked earlier: What do you love about flying the B737 at Southwest that you couldn’t get at another major?

Get Moving!

Our world, our country, and our industry are full of bad advice. Mine certainly isn’t perfect, but it’s at least better than the kinds of lies and part-truths that are holding far too many pilots from achieving better careers.

Don’t let arbitrary catch phrases or outright ignorant statements prevent you from moving on to an airline with superior Scope, QOL, and pay.

If you’re at a regional or a Tier 2 airline, you are competitive for one of the 6 (or 5 or 4) major airlines. Your family deserves a shot at the pay and QOL those companies offer!

Clean up your logbooks, resumes, and applications, and submit them! This is an unprecedented time in human history and your family at least deserves the opportunity to turn down an offer from a company that has the kind of Scope that gives you all the benefits and all the choices.

Flight training is a huge investment of time and money. You’re not the first person to wonder whether it wouldn’t just be cheaper to buy your own plane, hire a freelance CFI (or teach your own kid,) and then enjoy or sell the plane once your target audience reaches 1500 hours and/or gets a full-time pilot job.

You can make this work if you get the right aircraft with the right setup. However, it’s not the right answer for everyone. Let’s consider the factors:

Aircraft Choice

Since you’re doing this, at least in part, to cut costs, you must target the right kind of aircraft. You need something tried and true, familiar to every mechanic in the country, with lots of spare parts easily available from major suppliers.

You also need something simple. That means a fixed-pitch prop turned by a single engine, fixed landing gear, and 2 or 4 seats. No exceptions allowed. More complex aircraft just have more moving parts that need to be inspected (expensive) and have more opportunity to break (expensive, and prevent training for weeks or months until repairs are completed,) and require more expensive insurance.

Basically, this limits you to about three aircraft types:

The Cessna C-172

The Piper PA28 family (Cherokee 140, Warrior, Cherokee 180, Archer)

The Cessna C-152 (not the C-150)

Older C-172s were powered by the Continental C-145, or O-300. Having owned an aircraft with this engine, I think it’s a piece of junk. If you spend any time in any O-300 owners forum online you’ll hear constant complaints about maintenance issues. If you’ve been working on car or airplane engines for decades and/or can find an aircraft with a factory remanufactured or factory overhauled engine, you can consider an O-300. Otherwise, buy an aircraft with a Lycoming O-235, O-320, or O-360.

Yes, there will be thousands of other aircraft that fit your criteria and budget. Yes, many of them look cooler, fly faster, or cost less. It doesn’t matter. The FAA could care less how many miles a pilot has traveled. All FAA ratings are based on hours. If your airplane flies slowly, you just log more hours any time you go somewhere. This purchase must be about one thing: your mission.

That mission is: reliably flying as many hours as possible in the shortest possible amount of time, up to 1500 total hours per trainee. Allowing yourself to be distracted from that mission in any way only brings heartbreak, and large checks with your signature in the corner.

Avionics

Avionics are important and expensive to install. If you plan for this airplane to serve as an IFR training platform, you need to buy one that already has some upgrades. At a minimum, this means a pair of Garmin G5s or uAvionix AV30s serving as an ADI/PFD and HSI/MFD. Other good options here include products from: Aspen Avionics, Dynon, or the Garmin G3X.

If you’re doing IFR training, you also need an IFR navigation unit. The industry standard right now is the GTN650. It’s gorgeous, powerful, and very expensive. There are “cheaper” alternatives, designated GPS175, GNC355, and GTX375. They’re good enough for your purposes when paired with the appropriate legacy radios and/or transponder.

You will also see aircraft with the previous generation of Garmin’s IFR navigator, the GNS430 or GNS530. They’re fantastic products, but I’m not sure how long Garmin will continue to support them. If you can verify (directly from Garmin, not from the seller) that the unit will continue to receive database updates for at least the next year or two, they’ll be okay.

You can find the PFD/MFD options I mentioned at reasonable prices, and you can get a cheap GNS430 on eBay. You may be tempted to buy a plane with steam gauges and hire your own mechanic to install the new stuff…because it’ll be cheaper.

In general, this is dead wrong.

Installing these new avionics requires major surgery to your panel, wiring, and plumbing. Regular A&P Mechanic shop rates start around $75-100. Specialty avionics shops can quickly double that. You might see individual instrument sticker prices in the single-digit thousands and think they’re reasonable. It doesn’t take many shop hours at these rates for your final bill to more than double the sticker price of the boxes themselves.

We’ll discuss why later, but you must also consider the fact that you’ll probably spend months waiting for the shop to get your work done.

You aren’t reading this because you thought a couple years ahead. You’re reading it because someone in your family is ready to start flying right now. Best case: it’ll take you at least a few weeks to buy a plane in the first place. Then, you’ll have to find a shop willing to do your work, wait for all the parts and gadgets to be delivered, and also wait for them to be installed. You’re looking at a minimum of 6 months before your plane will be usable. In the meantime, you’ll have shelled out $10-30K over your aircraft’s purchase price. Ouch.

Yes, I know you found someone who promised to do things more quickly and for a better price. No, they aren’t intentionally lying to you. They’re just unrealistically optimistic. That misplaced optimism costs them nothing, but it costs you a lot. Again, more on why later.

Instead remember: you’re infinitely better off buying a plane with the avionics you need already installed.

2 x G5s or AV30s

GTN650 (or similar)

GNS430 (maybe)

Yes, there are great products from some other companies like Avidyne and Bendix/King. They’d work, but the only people who install them in a plane they’re selling are people who are trying to save pennies, while getting rid of something they don’t want, ASAP. Where else might they have skimped with that airplane, and how will that affect its reliability as a trainer for you?

Also, Garmin is the industry standard. You’ll actually find CFIs who are either reluctant to fly for you because of the unfamiliar avionics, or they’ll be less effective because they know less than you about how to use them.

It should go without saying, but you also need an airplane already equipped with a legal ADS-B Out solution. One exception to my “don’t plan to upgrade” rule is the uAvionix tailBeacon, a surprising instance of a quick, easy, cheap solution. This unit works with existing transponders, costs about $2000, and any A&P can install it in less than two shop hours. This means you are allowed to consider an aircraft that doesn’t already have ADS-B, as long as it’s otherwise perfect.

Stay on Target

At price ranges that make sense, you’re looking at aircraft produced in the 1960s or 1970s. You can find newer C-172s and Cherokees, and they’re good options, as long as you’re willing to spend more. (I’ve recently seen later-model C-172s in the $200K-300K range. It’s completely absurd, but it’s the reality of today’s market.)

The catch is that with all the other expenses of aircraft ownership, you’ll rapidly reach the point where it’s cheaper to spend $100K for an accelerated zero-to-hero flight training program at a big-name school and get a job as a CFI the moment you graduate. We’ll run some actual numbers later.

As you start shopping, you’ll come back and tell me that for just a little more money you can get a nicer, newer aircraft like a Diamond DA20 or DA40, or a Cirrus SR20. They’re all proven trainers. However, they’re also more expensive. Even at the top of your budget, they aren’t likely to be newer enough to be more reliable.

If you’re thorough, you’ll also notice options like Piper’s PA20 Pacer or PA22 Tri-Pacer, and Cessna’s C-140 or C-170. Unfortunately, these aircraft are just too old for your mission. They’re worn out. Many have original wiring from the 1940s or 1950s. Parts are increasingly rare, if accessible at all. These are wonderful aircraft for enthusiasts who have the time and means to work on or (better yet) restore them.

That is not your mission.

Why So Militant?

I’ve only owned two aircraft so far, but you could say I’ve been “studying” this art for decades. I’ve worked with or hired A&P Mechanics from all over the US. I’ve advised and helped owners of a very wide variety of aircraft.

Let’s think about the type of vehicle we’re buying: If you were to spend $50,000-$100,000 on a car produced in the 1960s or 1970s, how would you treat it?

In most cases, you’d act like Cameron Frye’s dad. You’d never drive it. You’d just rub it with a baby diaper. You’d take it to car shows and meetups. You might do the occasional drive for a few hours on a weekend. If you really trusted your kid, you might let them drive it to a special occasion like prom. (Stay out as late as you want, do whatever you want somewhere else, but the car must be in the garage by midnight!) You certainly would not use this car as a daily driver for a long commute.

And yet, that last case is exactly the mission for your airplane.

“It could get wrecked, stolen, scratched, breathed on wrong… a pigeon could shit on it! Who knows?” You can’t afford to treat your plane that way.

Why wouldn’t you drive an older car that much? Well, it’s old! This means the more it drives, the more maintenance it requires. Those parts aren’t getting produced anymore, so they’re only getting more expensive. You didn’t buy this car to keep it at your mechanic’s shop. You bought it to keep at your glassed-in show garage. Even if you’re a car guru who can do all the work yourself, you don’t actually want to spend all your time working on it. You’d like to drive it sometimes too.

You have to consider similar factors with your airplane, except you don’t have the luxury of just letting it sit in the hangar. The only reason to buy it was to put it to work. You’re going to spend just as much on this plane as you would on a vintage muscle car, but you’re getting the equivalent of a 1980s Dodge Caravan. However, the fixed costs of owning an airplane are way higher than those associated with owning a classic car.

You’re stuck with this option because used aircraft prices are already insane. The 60s or 70s Cessna and Piper spam cans are the best balance of capability, reliability, insurability, and price. You can still find parts, any A&P will work on them, and they have a history of reliability that should keep them out of the shop. Anything fancier or faster and you have to sacrifice some or all of those benefits.

Why Such Focus on Maintenance?

For me, maintenance has been the most frustrating part of aircraft ownership. Airplanes, especially trainers, work hard. Unfortunately, most pilots lack the mechanical savvy to care for their machines as well as they could.

If you buy a used aircraft, especially one that’s been owned by numerous people over numerous decades, there will be a lot of deferred maintenance or updates. Worse, it will be difficult to know about them before you buy. (We’ll look at how to improve your chances with that in a bit.)

If your airplane gets grounded for maintenance, it’s useless to your trainee until it gets fixed. In this day and age, once a person starts flight training, it behooves them to complete that training as quickly and efficiently as possible.

They need to get to their first paying pilot job so they can stop paying for their own hours. They need to get to the regional airlines quickly so they can start building turbine time. Everything should be focused on getting to the really great jobs at major airlines. On some level, everything else is just grind.

Everyone knows that there’s a pilot shortage in our country, but not everyone realizes that the aircraft mechanic shortage is much worse. This isn’t a glamorous job. A&P school is long and expensive, but it doesn’t include a college degree. Many people look down on it and/or think that it doesn’t pay well. (Both of those opinions are stupid and wrong.)

As such, every aircraft maintenance shop in the country has far more work than they can handle. Sure, they’ll agree to work on your aircraft. Most of them will even give you an honest estimate and do good work…when they get around to it.

The problem is that when you bring your airplane in for a job worth $900 to chase brake issues, or even the $10-30K we mentioned for an avionics upgrade, you’re not a very lucrative client. Since demand for maintenance is through the roof, your shop will always have another Bonanza waiting for a $75,000 avionics upgrade or a Baron with $125,000 in engine changes.

That shop is financially better off finishing those lucrative jobs first to get more cash through the doors. They’ll take care of your piddly $2100 uAvionix tailBeacon install when they get a chance.

Definitely this week.

Oh, except they just got a Saratoga in for an annual inspection that’s going to run at least $15,000.

Definitely by the week after that though.

Sadly, this never ends.

Does it frustrate you? That’s okay. You’re welcome to try another shop next time.

We small-time aircraft owners won’t ever win this one.

This is why you need single engine, fixed-pitch propeller, and fixed gear. You need something that has the fewest number of things possible to go wrong. And when they do, you need them to be something that your mechanic is familiar with and can do quickly, when they get around to it.

Airplane Shopping

I have three favorite places to shop for airplanes:

FLYING Magazine is launching a marketplace that has some potential. If you want access to the beta, hit up Preston Holland on LinkedIn. If you’re looking for a glider I like the classifieds at Wings and Wheels.

Go. Shop. Enjoy.

Trade-A-Plane is one of my go-to resources for airplane shopping.

As you do, remember that classified ads are like online dating profiles. Pictures were taken on the best hair day ever, right after a muscle-toning workout, with any belly sucked way, way in…probably a few years ago. Profile details are…optimistically…true, but you’re always going to be a little surprised when you actually meet in person.

I’ve gone to look at many airplanes that I (thankfully) didn’t buy because even my non-mechanic eye could see issues too expensive or difficult to fix to make the asking price reasonable.

Also realize that you will fall victim to a phenomenon I call “mission creep.”

You’ll be shopping for that reasonable C-152 when you realize that for “just a few thousand dollars more” you could get a 4-place plane like a C-172. A few shopping minutes (or hours) later, you’ll realize that for “just a few thousand dollars more” you could get one with the nicer IFR avionics I mentioned above. Then, you’ll realize that for “just a few thousand dollars more” you could get something a little bigger, a little faster, a little cooler, etc. Soon, you’ll find yourself looking at C-310 twins and TBM-700s.

When (not if) this happens, you need to push away from the computer for a moment and realize that you’ve exceeded your mission parameters. Start all the way back over at C-152s and try again. Don’t feel bad about this. Mission creep happens to me every time I shop.

Always focus on finding the best value for your mission.

Fundamental Criteria

Aside from the types of aircraft and avionics we specified above, a few easy criteria can quickly rule out an airplane, or show that it warrants further consideration.

Engine Time

The engines you should be considering (O-235, O-320, O-360) have a Time Between Overhaul (TBO) of 2000-2400 hours, depending on the model. As long as you’re not a charter operator, you can fly an engine past TBO.

A motor with a very recent overhaul is actually the worst deal, even though sellers charge the most for them. Overhaul quality varies…significantly. A “zero-time” motor with a shitty overhaul is nothing but an expensive Pandora’s box. You want at least 300 hours on an engine so the A&P doing your pre-buy inspection (more on that later) can know if the motor was broken-in properly and how it’s actually running post-overhaul.

Overhauls are expensive; however, I’d be tempted to pay a lot less for an engine near or past TBO and pay for a top-shelf overhaul myself (or just replace the engine with a new one.) That way I’d know what I’m getting. Just realize that this means several months of your airplane sitting in a hangar without flying.

If you have the time to wait, and the $35K-50K to invest above purchase price, this is actually a great way to get a deal. If not, look for a “mid-time” engine with not less than 300 hours. Important terminology here includes:

Time Since Major Overhaul (SMOH) – the number of hours since a full overhaul was done. There’s no formal definition for a major overhaul, and quality varies. That’s why you don’t want a plane with a fresh one.

Time Since Factory Remanufacture (SFRM) – sending a motor to the factory is the best option short of just buying a new motor. The quality is all but guaranteed. Watch for sellers claiming a factory reman that wasn’t.

Time Since New (SNEW) – if this means an airplane’s 50+ year old is original without ever being overhauled, either plan to just buy a new one or run screaming from the building. However, if this means the seller opted to buy a factory new engine instead of doing an overhaul, this could be a great deal. You still need a qualified mechanic to confirm that.

Time Since Top Overhaul (STOH) – Again, there’s no definition of a “top” overhaul. This means the motor had issues. It’s possible that a great mechanic knew exactly the problem, replaced some cylinders and perhaps lapped some valves, set everything else back to stock configuration, and fixed everything. More likely, the owner was too cheap to do the full overhaul the motor needed. The mechanic earned a bunch of money treating symptoms, and you’ll have to deal with the underlying problems after your purchase. At best, this adds zero value to a listing in my book. More often, it’s a red flag.

Paint & Interior

Many otherwise bad airplanes have sold to unsuspecting buyers thanks to a gorgeous new paint job. Why did the seller pay $10K-15K to paint this 50+ year old aircraft right before trying to sell it? If it has new paint, you’re going to need a very conscientious mechanic to do a lot of looking inside the aircraft structure for things like corrosion or hidden damage. Don’t let outer beauty distract you!

A nice, new interior isn’t as much of a concern. This part really is only skin deep, and is made to be removed for inspection. Your mechanic will be able to see past this, so it could be a bit of a bonus. (A nice, new interior will cost you $5-10K.)

In both cases, the logbooks should make it very clear how recently these things were done. If the updates happened 5 or more years ago, there’s a better chance they aren’t trying to hide anything. If they’re less than a year old, or worse, in the paint shop right now, I’d need some compelling reasons to continue considering that aircraft.

Damage History + Logbooks

When I see an ad that says “no known damage history” I almost always close it and move on. Why don’t they know? Any damage should be in the aircraft logs. For me, this seller is trying to hide something.

That said, aircraft occasionally sustain damage. The damage and the subsequent repairs should be well documented. A good seller will be upfront about this. Most repair jobs are pretty easy for a mechanic to inspect. They can tell if the firewall is bent from a prop strike, if sheet metal is buckled or damaged, etc.

If the aircraft did experience a prop strike, either there should be an extensive report of the inspection that deemed the engine okay to continue in service, or records of an engine overhaul or replacement.